The latest Future Electronics Market Conditions Report (May 2026) provides a valuable snapshot of current supply chain conditions across the electronic component industry. While the broad market remains relatively stable, several product categories are experiencing increasing lead times, pricing pressure, and selective availability that warrant close attention. As always, this report serves as essential guidance for purchasing professionals and electrical/mechanical engineers navigating lead times, pricing pressure, and availability in a still-constrained environment.

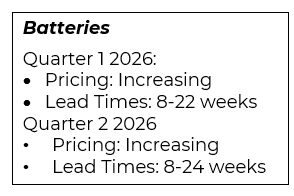

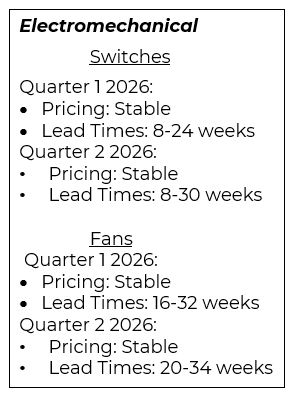

Battery supply remains generally stable overall, though selective pricing pressure is emerging. Within electromechanical components, the outlook is more mixed, with certain product categories showing signs of extended lead times and availability.

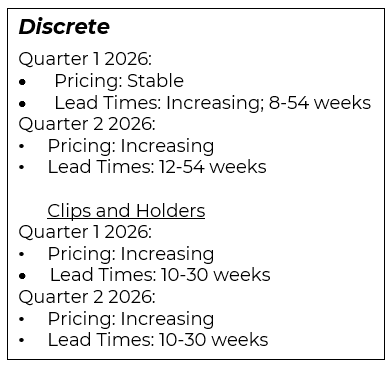

Discretes continue to be one of the most challenging categories in the current market, with widespread increases in both lead times and pricing across MOSFETs, diodes, transistors, and protection devices. Demand from industrial, automotive, and power-management applications continues to outpace supply in certain segments. Secure supply for new designs now.

- Purchasing: Aggressively forecast and place orders for MOSFETs (especially Low/High Voltage and Wide Bandgap), TVS/ESD protection, and Schottky/rectifier diodes. Multi-sourcing and buffer stock (where possible) are recommended for items with lead times of 20-24 weeks or more.

- Design Engineers: Review approved vendor lists and qualify alternate sources for critical discrete components. Review designs for opportunities to consolidate or derate components.

- Risk Level: High — Dicretes have transitioned from a relatively stable category to one requiring active supply chain management. Monitor for further extensions into Q3/Q4 2026.

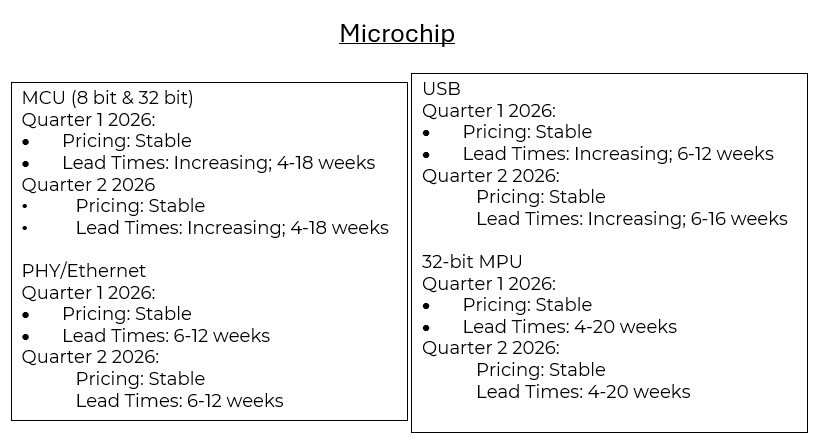

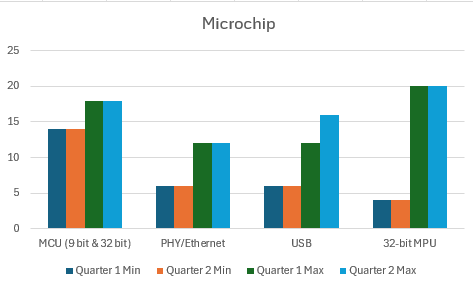

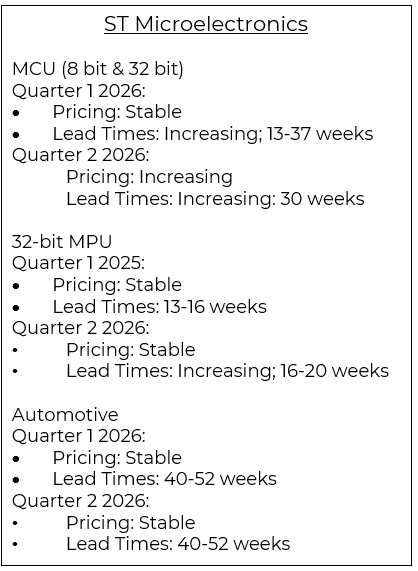

Overall, High-End MCUs, Ethernet/PHY, USB, and automotive-qualified parts remain manageable but require close monitoring for automotive and networking applications.

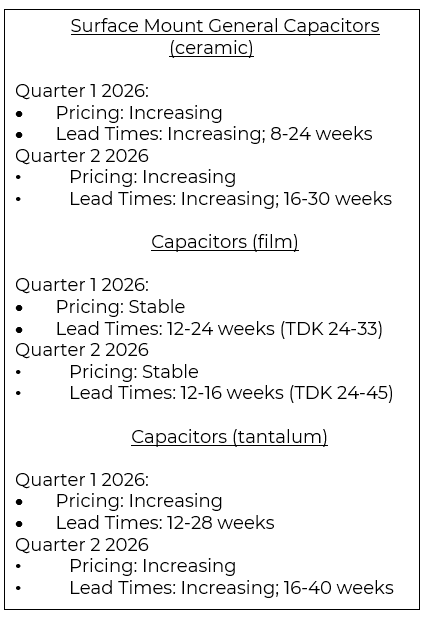

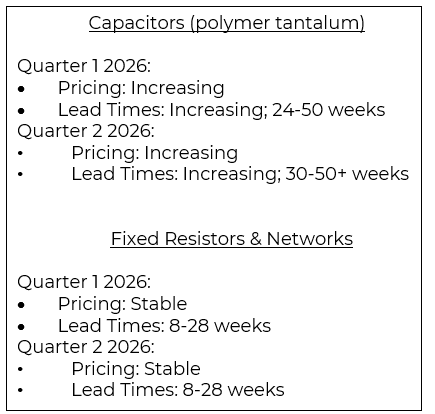

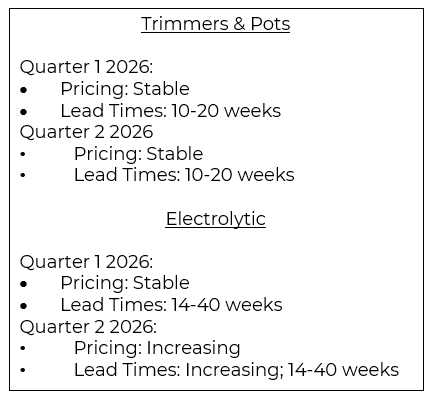

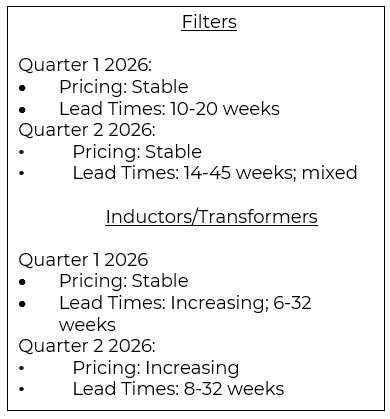

Passives remain a persistent area of concern, particularly in capacitors, where raw material costs (silver, tantalum) and capacity constraints continue to drive rising lead times and prices. The market shows selective tightness rather than uniform shortages, but certain sub-categories (Tantalum, Polymer Tantalum, higher-value Ceramics) are notably stretched.

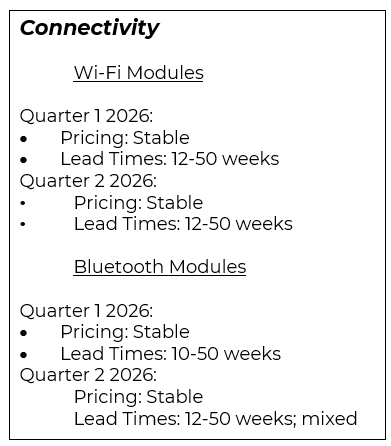

Overall, supply remains manageable for most standard modules, though longer-tail LoRa and cellular-integrated variants are more stretched. Purchasing teams should forecast early for high-volume or automotive-qualified parts.

The May 2026 market environment is best characterized as one of selective tightening rather than broad-based disruption. The greatest areas of concern remain discrete semiconductors, tantalum-based capacitor technologies, automotive-grade passive components, and selected electromechanical products. While many High-End MCUs, Wi-Fi/Bluetooth modules, and standard passives remain relatively available, upward pricing trends and extended lead times in critical areas underscore the importance of proactive planning. Purchasing professionals should focus on demand forecasting, multi-sourcing strategies, and inventory buffering for high-risk items, while design engineers are encouraged to review BOMs early for alternatives and flexibility. Organizations that combine proactive procurement strategies with flexible design practices will be best positioned to navigate the evolving component market through the remainder of 2026.

At Burton EMS, we go beyond contract manufacturing by offering value-added services that support smarter planning and supply chain resilience. From engineering services to support new or revised designs to setting up bonded systems for large volume components, our team helps you stay ahead of market dynamics. Visit our website to learn more about how we can add value to your next project. www.burtonems.com